What is all of the hype about a memory shortage and, in short, what do procurement professionals need to know to manage the latest crisis?

High-bandwidth memory (HBM) demand driven by AI infrastructure is materially constraining all global memory supply. Leading manufacturers, like Samsung, SK Hynix, and Micron, are reallocating production capacity away from traditional DRAM and NAND toward HBM, tightening supply for commodity memory products. The result is rising prices, longer lead times, accelerating obsolescence, and increased procurement risk through at least 2026. Listed below are bullet points explaining the concerns we think matter most for procurement professionals.

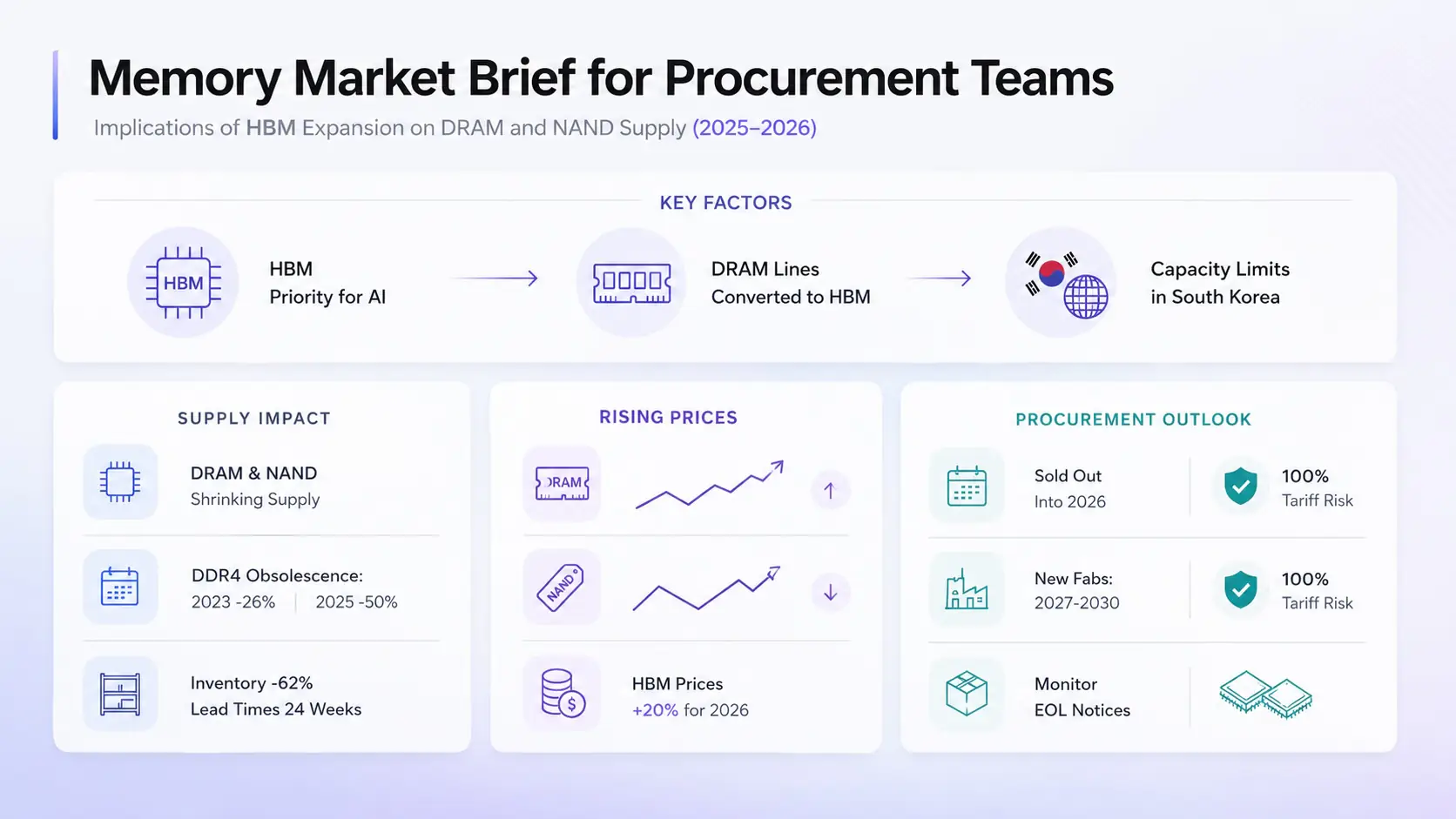

What’s Driving the Shortage

- HBM is now the top priority for memory manufacturers due to AI accelerator demand and higher margins.

- Production tradeoffs are real: In some cases, DRAM lines are being physically converted to HBM; in others, future capex is directed almost entirely to HBM expansion.

- HBM capacity is nearing limits, especially in South Korea, where the majority of advanced memory production is concentrated.

Supply Impact on Traditional Memory

- DRAM and NAND supply is shrinking despite steady or growing demand from automotive, consumer electronics, telecom, cloud, and industrial sectors.

- DDR4 obsolescence is accelerating:

- 2023: 26% of DDR4 MPNs are obsolete

- 2024: 33% obsolete

- 2025: 50% obsolete

- Inventory contraction is severe:

- Top manufacturers’ available inventory fell 62% in six months (June–December).

- Lead times have nearly doubled, moving from 12 weeks to 24 weeks on average.

Pricing Signals

- Commodity memory prices began rising in late 2024, accelerating sharply in mid-2025.

- DRAM prices increased ~172% year-over-year by Q3 2025, according to media reports.

- Samsung and SK Hynix have raised HBM prices on average 20% for 2026 deliveries, reinforcing the incentive to prioritize HBM over commodity memory.

- Samsung has slowed its DDR4 phase-out, not due to recovery in supply, but because prices have surged amid scarcity.

Near-Term Outlook (2025–2026)

- Memory makers are sold out well into 2026 for certain products.

- New capacity is coming, but not soon enough:

- Micron fabs in Idaho: production begins 2027–2028

- New York fab: expected ~2030

- Trade and policy risk are increasing, with the U.S. signaling potential tariffs of up to 100% on imported memory if manufacturing does not shift domestically.

Procurement Implications

- Expect continued tight supply and elevated pricing for DRAM and NAND through at least 2026.

- Legacy parts (especially DDR4) face rising EOL risk. Design-in alternatives early.

- Spot buying risk is high; pricing volatility favors contracted supply.

- Pull-ins are already occurring, especially among PC and electronics OEMs, further stressing availability.

Recommended Actions:

Lock in longer-term supply agreements and increase buffer inventory for critical parts. AERI can buy, hold, and schedule for you.

- Actively monitor EOL notices and MPN reductions

- Qualify second sources or newer memory generations early

- Budget for structurally higher memory costs, not cyclical reversion

Don’t let hard-to-find electronics jeopardize your bottom line.

Is a Single Component Slowing You Down?

Contact your search expert at www.aeri.com today to Solve Your Hard-to-Find Component Challenges

Robb Hammond is the founder and CEO of AERI, an independent electronic component distributor operating since 1994. He is a founding member and former committee chair of SAE AS6081, the counterfeit-avoidance standard for independent distributors adopted by the U.S. Department of Defense, and a recognized authority on counterfeit detection.